High quality bonds in the spotlight

April 10, 2020 - 2 minutes read

Posted by James Spencer

There is an old adage in the investment world that ‘diversification is always having to say you are sorry’, as there is usually one (or more) parts of the portfolio that is a bit disappointing. Every asset class has its day in the spotlight, for good or for bad, at some point.

Over the past couple of years, shorter-dated, high-quality bonds that constitute strong defensive assets have delivered low returns and have had a finger pointed at them, by some. Bond yields have been at historical lows, with yields on 5-year UK government gilts at or below 1% for the past three years. Today they stand at around 0.2% and that is before the impact of inflation. It is understandable that investors find low yields frustrating, but one needs to look at the bigger picture. Bonds sit in long-term portfolios predominantly to provide some stability at times of equity market turmoil.

In the face of these low yields, investors have had two straight choices: accept the fact and stoically maintain the quality of their bonds; or go in search of yield by owning lower credit quality bonds and/or bonds of longer maturity. We know that many have been tempted by the latter strategy. We have stuck to the former to defend the portfolio at times of equity market turmoil such as this. Remember that the lower the credit quality of bonds, the more they act like equities.

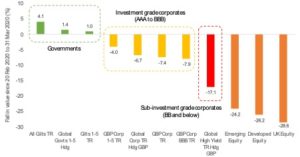

We think of yield-driven bond strategies – particularly high yield bonds – as akin to picking up pennies in front of a steamroller, which works nicely until you trip over. The chart below looks at the performance of different types of bonds since the equity markets began to fall in February this year.

Figure 1: Bonds do not all perform the same at times of equity market turmoil

Source: Albion Strategic Consulting. Data: see table overleaf for indices used. © Morningstar Direct. All rights reserved. Note: 1-5 = bonds with maturities between one and five years (i.e. short-dated)

It reveals that high-quality bonds have more or less held their value, doing the job asked of them. As one moves down the credit spectrum to lower quality companies, returns become increasingly negative. Owning these lower quality bonds, but with longer maturities, simply magnifies these falls (heading from left to right in the chart). As it has always done, scared money runs from higher risks (including the possibility of default on bonds from less healthy companies) which drives yields up and prices down. It tends to move into high-quality, liquid assets driving bond yields down and prices up.

As Warren Buffet once said:

‘Only when the tide goes out do you discover who’s been swimming naked.’

Fortunately, your portfolio has kept its trunks on!

Head of Investment at Xentum – Tim Hale

Also you may be interested in looking back over some of our historical articles that may give you some food for thought.

Budget Summary – Got lost in all the mayhem but still very relevant

Click Link:- Budget update March 2020.